An inventory report is a summary of items belonging to a business, industry, organization, or home. It provides a comprehensive account of the stock or supply of various items. They can be written in various forms and lengths. A good inventory report should always be clear, simple, and exhaustive.

For many types of businesses — including retailers and manufacturers — inventory is typically a leading source of collateral. But you can’t always accept inventories at face value, because borrowers may use different accounting methods to report their inventories. Before committing to a deal or when reviewing an existing customer’s financial performance, it’s important to understand how the company reports its inventory.

The basics

Borrowers that sell unique and expensive items — such as custom homes or jewellery — are likely to track each item in inventory separately. But most companies sell large amounts of similar items that would be impossible to track individually, so they make assumptions about how costs flow through their accounting systems. While there are variations within these broad themes, borrowers typically report inventory using one of these methods:

First-in, first-out (FIFO): As the name suggests, the first products that a company purchases (or manufactures) are the first to be expensed as cost of sales under this method.

Last-in, first-out (LIFO): This method essentially works in the reverse of the FIFO method. The most recently purchased (or made) inventory items are first to be expensed to cost of sales.

Conversely, some borrowers opt to use the weighted-average cost method, which basically splits the difference between FIFO and LIFO. It assumes that all inventory items are sold simultaneously. It’s most common among businesses with inventories that can’t be differentiated, such as chemical manufacturers or refiners.

FIFO

The FIFO method is favoured by most foreign companies and multinationals, in part because LIFO is banned by International Financial Reporting Standards. But it has advantages for domestic companies, too.

By expensing its oldest purchases first, a company that uses FIFO typically reports lower cost of sales and, therefore, reports higher profits (and taxable income) than if it had used LIFO. In addition, a company that reports inventory using FIFO will report higher inventory values, because items purchased later are still on the books. Both of these advantages assume, however, that the company is operating in an inflationary environment in which prices increase over time.

The reverse can happen when prices of goods, labour and other inputs decrease. These ups and downs can potentially distort profits. It’s important for a banker to understand how FIFO works, as well as track industry pricing trends, to gauge the potential for distortion.

LIFO

If the FIFO method enables a borrower to boost profits and collateral values, why would anyone choose the LIFO method? The key advantage to LIFO is its income-tax-saving opportunities.

Again, assuming that inventory and its related costs typically increase over time, LIFO generally results in lower profits and taxable income. That’s because the company’s most recently acquired inventory items (with presumably higher values) are expensed first.

By shifting its higher-cost inventory into the cost of goods sold and retaining its lower-cost inventory on the balance sheet, a company reduces its taxable income. This method may reduce a company’s income tax liability (at least temporarily), which, in turn, increases cash on hand to spend on new inventory purchases or other investments.

The downside, of course, is that a borrower that uses the LIFO method will generally appear less creditworthy than an otherwise identical borrower that uses the FIFO method. The perceptions of diminished profitability and less valuable collateral could make it harder, but not impossible, for a company that uses LIFO to secure debt and equity financing.

LIFO also can be more difficult to track, given the numerous cost layers this method entails. So, it may not be realistic for companies with limited accounting resources — or that operate under deflationary market conditions — to use this method.

Explaining the LIFO reserve

Borrowers often use the first-in, first-out (FIFO) method for internal recordkeeping but switch to the last-in, first-out (LIFO) method for external reporting, typically for tax reasons. If so, the company should have a LIFO reserve in place. This is the amount by which a company has deferred its taxable income by using LIFO.

Basically, the LIFO reserve (or allowance) is the amount left over after subtracting inventory costs calculated under LIFO from those calculated under FIFO. The reserve is generally a credit balance that will be applied against FIFO method inventory costs on a company’s balance sheet at the end of a reporting period, assuming that the company operates in an inflationary environment. If prices are decreasing or inventory is shrinking, the reserve will be reduced and could eventually have a negative balance.

The LIFO reserve may also cause complications if the company is sold, depending on how the deal is structured. In some cases, the seller may opt to liquidate its LIFO reserve, meaning that the seller would claim its LIFO reserve as ordinary income and pay taxes on it.

Awareness is a key

All inventory reporting methods have pros and cons. Borrowers often follow suit with other companies in their industry when deciding which method makes the most sense. Become familiar with your borrower’s inventory methods to verify that it’s the optimal fit and watch out for potential distortions to the borrower’s profits or collateral values

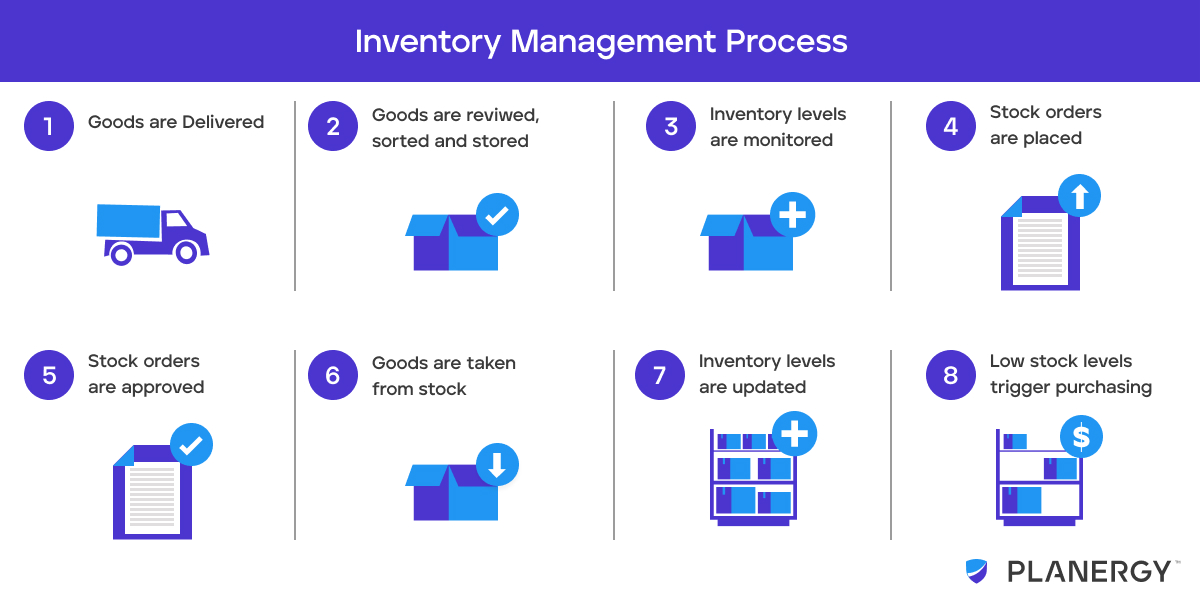

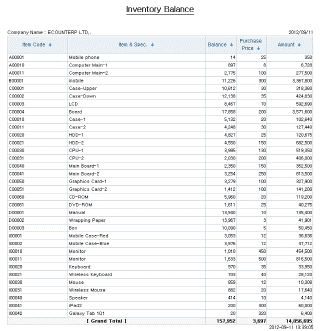

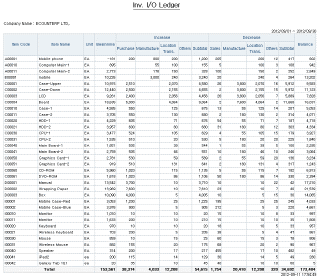

Inventory Reporting

To make accurate decisions, you need access to real-time data. Quickly check inventory and track incoming or outgoing items based on orders.

Inventory reporting is often a sore point for many businesses. Many complain the reports do not reflect real-time data in a manner that can be deciphered easily. As a result, businesses are left with thousands of dollars tied up in inventory that isn’t selling and taking up valuable space. Inventory management provides real-time, customizable reports that allow small and midsized businesses to take control of their inventory.

Common Issues

- Many managers feel reports don’t provide enough real-time information to allow them to make informed decisions.

- Lack of shared data between departments leads to errors, re-keying, and unreliable reports.

- No method to show inventory history and when data was gathered.

- Inventory management provides a variety of inventory reports users can access anytime, anywhere. The system is fully integrated with the sales, purchasing, and manufacturing departments to reflect the most current data without unnecessary re-keying.

Benefits

- Inventory reports to make informed decision in less time.

- With software in the cloud, users can access real-time reports anytime, anywhere.

- An integrated system reflects changes in sales, purchasing, and manufacturing departments in the inventory ledger.

- Customize the reports to show the factors that are important in your company.

Inventory Reports

Quickly search the inventory ledger

- Inventory movement is automatically reflected in the inventory ledger.

- Search by item type, location, serial number, group and more at any time with web access.

- Through the hyperlink function, you can trace back from a search screen to the first input screen.

Create professional, real-time reports

- Edit each field to company preferences.

- Add up to 50 fields in each report.

- Create reports without using Excel.

References

http://www.smith-howard.com/resources/articles/closer-look-accounting-inventory